- Investor Relations

- Financial Information

- Latest Results Announcement

Financial Information

Latest Results Announcement

Condensed Interim Financial Information For the Six Months and Financial Year Ended 31 December 2025

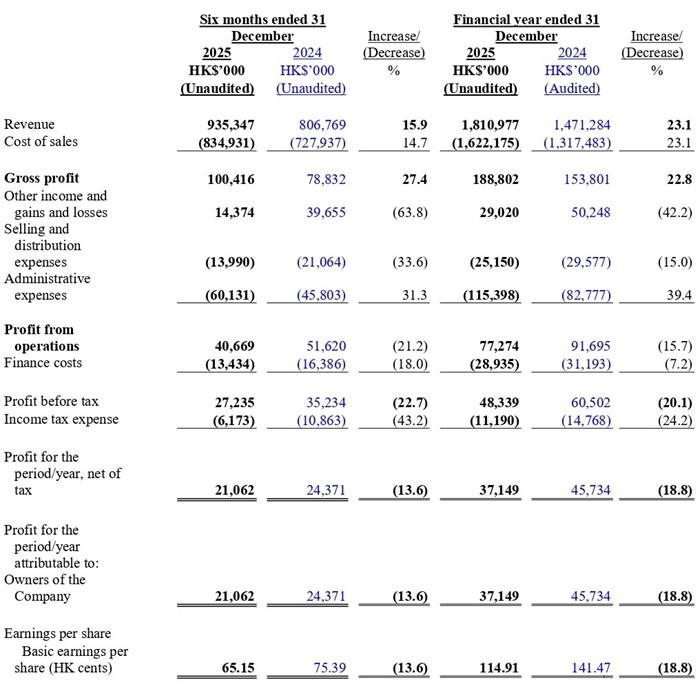

Condensed Consolidated Statement Of Profit Or Loss For The Six Months And Financial Year Ended 31 December 2025

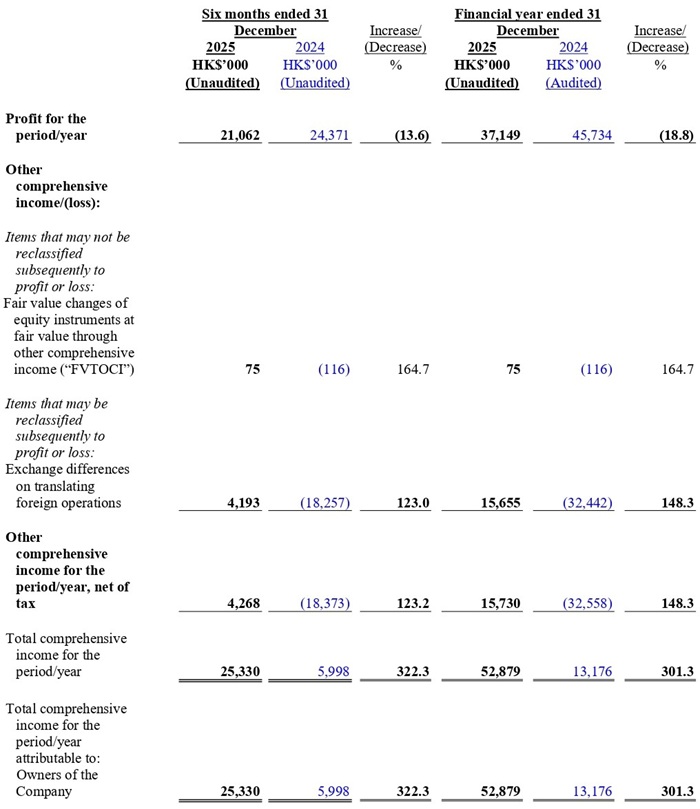

Condensed Consolidated Statement Of Profit Or Loss And Other Comprehensive Income For The Six Months And Financial Year Ended 31 December 2025

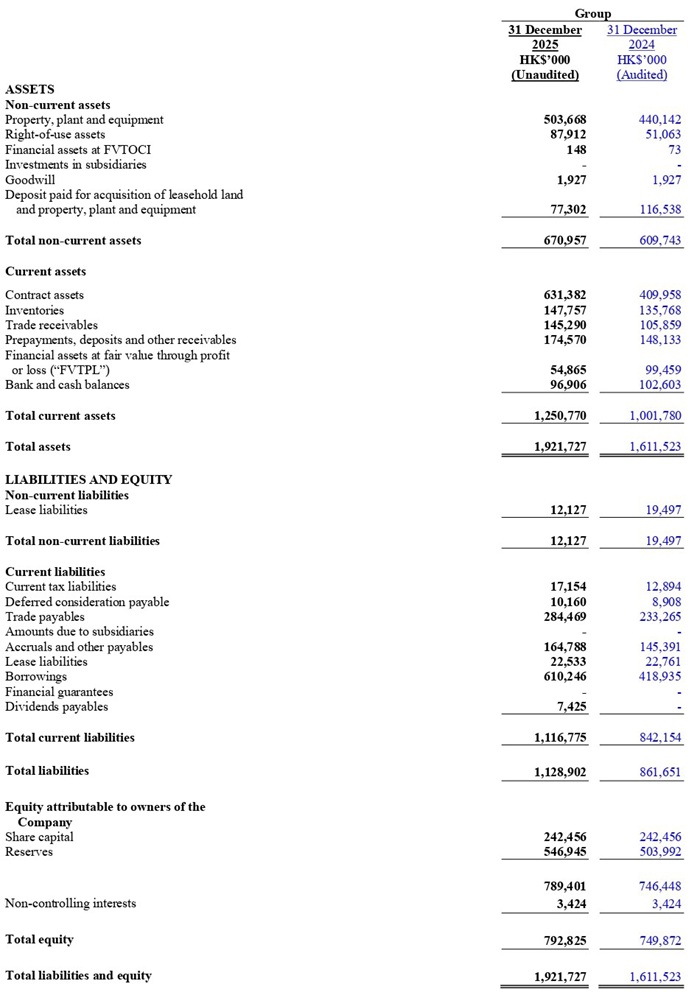

Condensed Statements Of Financial Position At 31 December 2025

Review of Performance

Profit and Loss

Revenue

The Group’s overall revenue increased by HK$339.7 million or 23.1%, from HK$1,471.3 million in FY 2024 to HK$1,811.0 million in FY 2025. The increase in revenue was primarily driven by an approximately 27% volume increase in orders from key customers.

Gross profit and gross profit margin

In FY 2025, the Group’s gross profit increased by 22.8% or HK$35.0 million, generating gross profit margin of 10.4% (FY 2024: 10.5%). This stems from our stable overall operations and the ongoing ramp-up of production capacity for high-margin products.

Other Income

The Group’s other income decreased by 42.2% or HK$21.2 million, from HK$50.2 million in FY 2024 to HK$29.0 million in FY 2025, mainly due to the non-recurring, one-off gain on disposal of Dongguan Shenshan factory of HK$23.4 million recognised in Dongguan during FY2024.

Selling and distribution expenses

The Group’s selling and distribution expenses decreased by 15.0% or HK$4.4 million, from HK$29.6 million in FY 2024 to HK$25.2 million in FY 2025. This was mainly due to the variations of the distribution of product destinations, which led to lower transportation costs and export fees.

Administrative expenses

The Group’s administrative expenses increased by 39.4% or HK$32.6 million, from HK$82.8 million in FY 2024 to HK$115.4 million in FY 2025. This was mainly due to daily operating expenses for newly commenced business unit in Indonesia, additional senior management for future development, professional consulting services on full-scale manufacturing and some non-recurring expenses.

Finance Costs

Finance costs decreased by 7.2% or HK$2.3 million, from HK$31.2 million in FY 2024 to HK$28.9 million in FY 2025, mainly due to the decline in HIBOR and the restructuring of our banking facilities, with a shift to banks offering lower borrowing interest rate.

Income Tax Expenses

Income tax expense decreased 24.2% or HK$3.6 million, from HK$14.8 million in FY 2024 to HK$11.2 million in FY 2025. This was mainly due to a 20.1% decrease in profit before tax.

Balance Sheet

Non-current assets

The Group’s non-current assets stood at HK$671.0 million as at 31 December 2025, an increase of 10.1% or HK$61.2 million, from HK$609.7 million at 31 December 2024. This was mainly due to:

- An increase of HK$32.7 million in deposits paid for the construction of the new factory in Indonesia;

- An increase of HK$63.6 million in property, plant and equipment for newly acquired equipment in Mainland China and Indonesia; and

- An increase of HK$31.8 million in right-of-use assets for land acquired for the new headquarters in Dongguan and the renewal of the factory lease in Mainland China.

which were partially offset by:

- Net effect of depreciation, disposal and exchange difference of HK$97.6 million.

Current assets

The Group’s current assets stood at HK$1,250.8 million as at 31 December 2025, an increase of HK$249.0 million or 24.9%, from HK$1,001.8 million as at 31 December 2024, mainly due to:

- an increase in contract assets of HK$221.4 million;

- an increase in inventories of HK$12.0 million;

- a decrease in trade receivables of HK$39.4 million; and

- an increase in prepayments, deposits and other receivables of HK$26.5 million.

which were partially offset by:

- a decrease in bank and cash balances of HK$5.7 million; and

- a decrease in financial assets at FVTPL of HK$44.6 million.

Current liabilities

The Group’s current liabilities stood at HK$1,116.8 million at 31 December 2025, increased by HK$274.6 million or 32.6%, from HK$842.2 million at 31 December 2024, mainly due to:

- an increase in short-term borrowings of HK$191.3 million to finance working capital requirements;

- an increase in trade payables of HK$51.2 million;

- an increase in accruals and other payables of HK$19.4 million;

- an increase in current tax liabilities of HK$4.3 million;

- an increase in deferred consideration payable of HK$1.3 million; and

- an increase in dividends payables of HK$7.4 million.

which were partially offset by:

- a decrease in lease liabilities of HK$0.3 million.

Non-current liabilities

The Group’s non-current liabilities stood at HK$12.1 million as at 31 December 2025, a decrease of HK$7.4 million or 37.9%, from HK$19.5 million as at 31 December 2024, mainly due to decreases in lease liabilities of HK$7.4 million.

Cash Flow Analysis

As at 31 December 2025, the Group’s cash resources of HK$96.6 million are considered adequate for current operational needs. The net decrease in cash and cash equivalents of HK$5.7 million held by the Group comprised:

- Net cash used in operating activities of HK$32.4 million to finance working capital needs;

- Net cash used in investing activities of HK$130.1 million mainly due to additions of deposit paid for new lands in Mainland China and property, plant and equipment in Indonesia and Mainland China; and

- Net cash generated from financing activities of HK$160.3 million, mainly due to the net borrowing of loans increased for the expansion mentioned above in investing activities.

Commentary

In FY2025, the Group delivered double-digit revenue growth of 23%, notwithstanding an increasingly complex global operating environment. The toy and premium products manufacturing industry continues to undergo structural shifts, including supply chain diversification away from single-country concentration, rising sustainability requirements from global brand owners, and heightened compliance and quality standards. Customers are placing greater emphasis on resilient multi-country manufacturing platforms, sustainable material applications and reliable execution capability. These industry developments continue to reshape competitive dynamics and favour manufacturers with diversified production footprints, strong governance frameworks and disciplined capital management.

During the year, the Group has made meaningful progress in strengthening its long-term positioning. The commencement of Plush Phase 2 operations in Indonesia, together with the ongoing development of the Group’s die-casting and plastic expansion projects, has enhanced its regional manufacturing platform and geographic diversification. The Indonesia expansion supports customers’ evolving sourcing strategies and is expected to contribute progressively as capacity utilisation improves. During the year, the Group also expanded its customer base and advanced discussions with potential new customers, further broadening revenue streams and enhancing business resilience.

Sustainability remains a key industry trend and competitive differentiator. The proportion of eco-friendly materials in the Group’s production reached a historical high level of over 77% in FY2025, exceeding the targets set in prior years and reflecting customers’ transition toward greener product offerings. While the adoption of sustainable materials may exert pressure on cost structures in the near term, it strengthens the Group’s alignment with global brand owners and enhances its long-term competitive advantage.

Looking ahead to the next reporting period and the coming 12 months, the Group expects industry conditions to remain dynamic. Geopolitical uncertainties, shifts in global trade dynamics and labour market pressures may continue to affect operating costs and supply chain stability. At the same time, the progressive ramp-up of Indonesia operations — expanding capabilities from plastic and paper to plush and die-cast production — will further strengthen the Group’s integrated manufacturing platform in Indonesia and enhance its competitive positioning. Continued customer diversification and the potential onboarding of new projects are additional growth opportunities. Following the significant capital expenditures undertaken in recent years to expand production capacity, the Group will closely monitor funding and capital expenditure commitments as Indonesia expansion progresses in 2026.